Greenlight

Product Name: Greenlight

Product Description: Greenlight is a prepaid debit card for kids that is funded via the parent's checking account. Assign and pay for chores in the app, or set transfers for a regular allowance.

Summary

The Greenlight app lets you assign chores to your kids and pay upon completion. You can also set up recurring or one-time allowance payments to the kid’s prepaid debit card. Prices start at $5.99 per month for up to five kids.

Overall

Pros

- Easy and safe way to give your kids spending money

- Simplifies chore management

- Investing available on higher plans

- Financial literacy content in the app

Cons

- Must upgrade from the basic plan to access investing features

- More expensive than similar services

Giving your kid regular spending money can be a pain. You don’t have cash when you need it, and you don’t really want your child walking around with a $20 bill in their pocket.

Greenlight has solved this problem with their debit card for kids. You can make instant transfers from your checking account to their debit card and have total control over where and how much they can spend. This gives you an easy, safe way to give your kids money and gives them a way to spend money on their own.

It’s not a traditional checking account; it’s just a debit card. If you are looking for a checking account, here are the best checking accounts for teenagers.

At a Glance

- Kids’ debit cards are funded by the parents.

- Transfers to kids can be tied to chores, which are set in the app.

- Parents can control spending amounts and block specific stores and categories.

- Pricing starts at $5.99 per month for up to five kids.

Who Should Use Greenlight

Greenlight is great for families with kids who need some spending money but shouldn’t be carrying cash. It’s also great if you want to pay for chores to get done but don’t seem to ever have cash on hand to actually give to your kids.

Greenlight Alternatives

| Pricing | $5.99 per month for unlimited kids | $5 per month for one child, or $10 per month for up to five kids | $4 per month for up to five kids |

| Free trial | 1 month | 1 month | 30 days |

| Chore management | Yes | Yes | Yes |

| Learn more | Learn more | Learn more |

Table of Contents

How Does Greenlight Work?

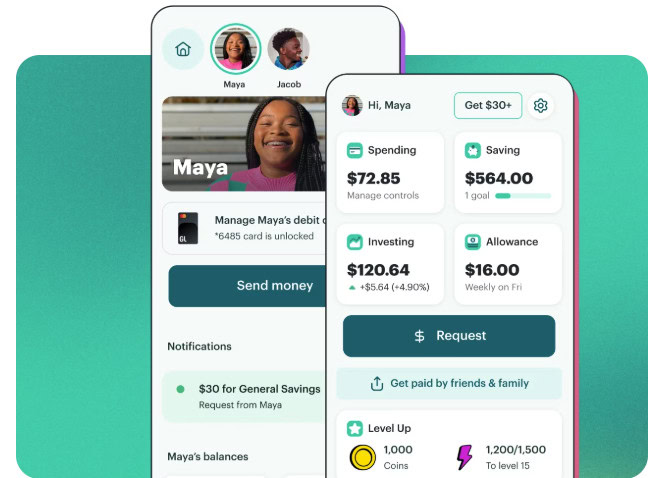

Greenlight is a prepaid debit card. You, as the parent, fund the card by transferring money from your linked checking account to each child’s card. Children of any age can have a debit card, and the monthly plans include up to five kids.

Everything is controlled on the app. You can assign chores that are paid once the child checks them off as completed. You can also set up automatic or one-time transfers for allowances that are not tied to chores.

You can also set spending limits for each child and receive notifications of transactions.

Greenlight Features

Chores and Allowance

This may be the most interesting feature of the Greenlight debit card. You can set up repeating and one-time chores and tie the payment of said chores to their completion. This can help motivate your kids and even show them the connection between work and compensation. The kids check off their chores on the app when completed.

You can also set up an automatic allowance. This is an automatic transfer from your checking to the child’s Greenlight debit card. It also doesn’t have to be automatic; you can transfer funds whenever you like.

Spending

Each child receives a Greenlight debit card to spend money. The card can be used in person, online, or at an ATM. You can also order a customized card with any image you want on the front. Card customization is a one-time fee of $9.99.

When your child makes a purchase, they can earn up to 1% cash back. This is deposited straight into their savings account. You can even round up purchases and transfer their spare change to savings.

Parental controls include setting spending limits and blocking specific retailers or entire categories of spending. For example, you could block spending at Game Stop or set aside a specific amount you’ll allow at that retailer. You’ll also get notifications when transactions occur so you can monitor things.

The Greenlight debit card is a MasterCard that can be used for both online and in-store purchases or anywhere else MasterCard is accepted. Although it may not be necessary, the card can be used in more than 150 foreign countries. It can even be used in conjunction with both Apple Pay and Google Pay.

Greenlight Financial Technology issues the Greenlight debit card, which has a Better Business Bureau rating of “B+” on a scale of A+ to F.

Saving

Savings accounts earn interest on the first $5,000 in savings (per family). The amount of interest depends on your plan, but it will be between 2% and 5%. Parent-paid interest is also an option.

Your child can set savings goals and watch their progress on the app.

All funds held on deposit are FDIC-insured through Community Federal Savings Bank. Greenlight uses reasonable administrative, technical, and physical security measures to protect personal information.

Investing

Kids can invest with no trading fees within the Greenlight app. Trades start at $1, and you must approve every trade. Kids make suggestions, but you must actually complete the trade. They can trade all stocks and ETFs on the New York Stock Exchange.

The brokerage accounts are held in the parent’s name, and the parent is responsible for all taxes.

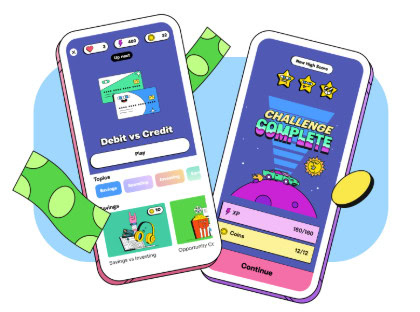

Financial Education

Within the app, there are bite-sized financial lessons and a game called “Level Up.” Level Up has engaging games with rewards for playing. It teaches kids about budgeting, credit, saving, spending, investing, and more.

Family Safety

With Greenlight, your family can share locations and receive SOS alerts and crash detection notifications.

You can even receive trip alerts. You can receive a notification when your teen has begun driving and then another when they arrive at their location. This notification includes a driving score and other details about their trip, such as if they exceeded the speed limit.

Greenlight also provides phone, purchase, and identity theft protection. (Phone protection is not available in New York.)

Greenlight App

The Greenlight app is the control center for all of Greenlight. Each parent and child will have their own log in and app experience. The app is where you’ll transfer funds, set your parental controls, set and approve chores, and approve trades.

The Greenlight app is available on Google Play and the App Store. It’s compatible with iPhone, iPad, and iPod touch.

Greenlight Pricing

Greenlight has three pricing plans: Core, Max, and Infinity. Each monthly price includes up to five kids and you’ll get a 30 free trial.

Core: For $5.99 per month, you’ll get all the basics of Greenlight. Up to five kids will each get a debit card and you’ll be able to set chores and allowances for each child. They will also have access to Level Up, the financial literacy game.

Kids will earn 2% interest on their savings accounts.

Max: For $9.98 per month, you’ll get everything in Core, but you’ll add on the 1% cash back on debit card purchases and the investing features. You’ll also receive protection for identity theft, purchases, and phones.

Kids will earn 3% interest on their savings accounts.

Infinity: For $14.98 per month, you’ll get everything in Max, but you’ll add on the family safety features.

There are two additional fees:

- $9.99 for a custom card (completely optional)

- $3.50 for replacing a card ($24.99 for expedited delivery)

There are no fees for making purchases, withdrawing money from an ATM, requesting a balance at an ATM, contacting customer service (automated or live agent), or an inactivity fee. If you are traveling internationally, there are no foreign transaction fees either.

Referrals

If you refer friends, and they sign up using your referral link, you can earn up to $600. Each friend you refer will also earn $30.

- First friend – $30

- Second friend – $50

- Third friend – $70

- Fourth friend – $150

- Fifth friend – $300

To find your referral link, go to the app and click on “settings” then “Refer a friend.” From that page, you will see a referral link to copy and send via email or text. Your friend must access Greenlight via that link and sign up. Once they have been a customer for 35 days you will receive your referral bonus.

Sign up for Greenlight

To sign up, you’ll need to provide your email address, mobile phone number, name, mailing address, date of birth, and Social Security number. You’ll also need to provide your children’s names.

Once you are signed up, you’ll connect the Greenlight account to a valid debit card or bank account.

Greenlight Alternatives

The Greenlight debit card is not the only debit card for kids available.

Some of the more popular alternatives include:

FamZoo

FamZoo is a prepaid card that works similarly to Greenlight. You can send money to your child’s card for them to spend. This will give you control over exactly how the card is used.

You can add money to the card and sets rules for how and when it can be received, such as by tying payments to tasks or chores. Alternatively, you could also set up automatic payments to act as payroll or allowance. You can even set up penalties if a child doesn’t follow the rules, such as completing their required chores.

When you use FamZoo, you don’t need to have a bank account linked to your FamZoo account – you can load it with cash or fund it with a direct deposit from an employer or government program.

FamZoo provides prepaid cards for your whole family at a fee of $5.99 per month for all family members. However, they do offer discounted fees if you pay in advance, as low as $2.50 per month if you pay 24 months in advance.

One of the benefits of a FamZoo debit card is that each has its own routing number and account number, which means you can set up both direct deposit or bank transfers to the card. You can even set each child up with several cards for different goals, including specific spending goals.

(Here’s a head-to-head comparison between FamZoo and Greenlight if you’re picking between the two)

Here’s our full review of FamZoo for more information.

Acorns Early

Acorns Early also offers a prepaid MasterCard that can be used anywhere MasterCard is accepted. The fee is $5 per month for one kid or $10 for the Family Plan, which has up to four kids, and you can cancel at any time. You can set up automatic allowance transfers, and set required tasks and chores to be completed.

You’ll also have a choice over where the card can be used, including specific stores, online, or at ATMs. You’ll receive real-time notifications each time the card is used, and you’ll also be able to block and unblock the card instantly. You can even set savings goals for your child. The entire account is managed from the Acorns Early mobile app, which is available for both iOS and Android devices.

Like other cards, you can set spending limits and savings goals and even give charitable donations.

Here’s our full Acorns Early review for more information.

BusyKid

Earnings are accomplished by completing chores, with “compensation” coming from you as an allowance directly deposited into the account each Friday — once approved by you. You can even pay bonuses through the card for good performance, like getting good grades or helping with a special project.

A percentage of that allowance can be allocated for automatic savings. The app can also be set to donate a percentage of the allowance.

Spending is accomplished through the BusyKid VISA Prepaid Spend Card. The app costs only $4 a month and includes one card each for up to five kids. It is accepted anywhere that takes Visa cards.

Summary

Getting your child their own debit card can take one of those little hassles out of life. Never again will you struggle to pay your kids their allowance, or worry about them losing your cash when they go out with friends.

Plus, a service like Greenlight gives you total control over where they can use their debit card and how much they can spend at particular stores. You also get access to where the card has been used–giving you control and security.