When Netflix started, they changed the game when it comes to streaming video online. Nowadays, there are a million streaming options like Hulu, Disney+, Paramount+ and Peacock.

As the OG of streaming, there are still a tricks to maximizing the value out of the service.

Netflix has been increasing prices to match its massive investment in original content. Subscribers now pay $15.49 per month for high-definition streaming on two screens. The basic version, for $6.99 a month, gives you only 1 screen in standard definition plus ads. Premium will cost you $22.99 but comes with Ultra HD and 4 screens at the same time.

Now, more than ever, you’ll need some of these Netflix hacks to save money and get the most out of your Netflix account! (especially if you’re cutting your cable and supplementing with them and services like DirecTV)

This post begins with a few suggestions on how to save money on your account and then goes into all the different undocumented “features” Netflix offers, from adjusting your streaming to seeing who is watching what (and you might be surprised!).

Table of Contents

- Buy Netflix Gift Cards

- Put your membership on “Hold.”

- Double Check Who Is Watching

- What’s New on Netflix?

- Manually Adjust Netflix Streaming Settings

- Review & Delete Your History

- How to Clear Your “Continue Watching” List

- Browse Hidden Genres

- Want some keyboard hot-key shortcuts?

- Netflix Doesn’t Have It?

- Need a Fireplace?

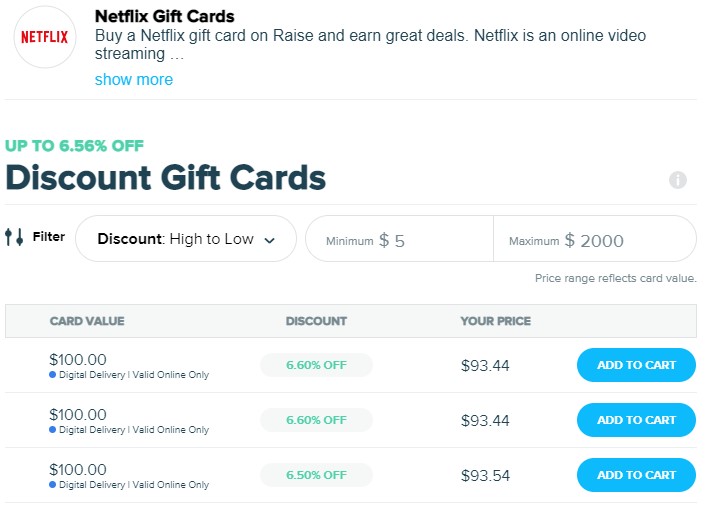

Buy Netflix Gift Cards

Gift card marketplaces like Raise will have Netflix gift cards on a huge discount. Buy a card and then apply it to your account for instant savings!

If that’s not still available, you can visit a marketplace aggregator to compare across multiple marketplaces. These rates change all the time, based on what people are trying to sell so shop around.

To apply your gift card to your account, go to My Account and enter the code into the form at the bottom of that screen.

At the moment, Raise has digital gift cards for 6.60% off – you could get a $100 gift card for just $93.44. Plus they also have sitewide discounts too (15PERCENT gets you 15% off to a maximum of $20 for new users):

The code arrives via email, copy and paste into your account, keep watching for less!

Put your membership on “Hold.”

In the past, you could pause your Netflix membership for any reason for a short period of time. Billing would stop and reactivate once the hold period ended. Netflix did away with that feature but you can still put a hold, it just requires a few more steps.

To pause your Netflix membership, you’ll need to cancel it and reactivate it. To cancel, go to My Account and click the Cancel Membership button underneath Membership & Billing. To reactivate, log back in within 10 months and update your payment information.

As long as you come back within 10 months, your account information (profiles, history, etc.) will be saved. If you dilly dally, it’ll be erased.

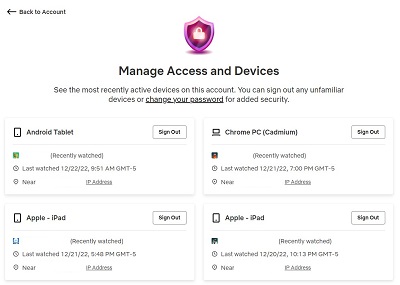

Double Check Who Is Watching

Your Netflix account is valuable and people’s accounts are being hacked all the time and traded in the darker portions of the internet, according to a McAfee report. (the report is kind of scary!)

Check your Recent Account Access page for any suspicious behavior or strange logins. If you do, sign out of all devices and change your account password immediately.

What’s New on Netflix?

There are a lot of browsing tools to help you find the latest and greatest on Netflix. My favorite is Instant Watcher, which will give you all sorts of ratings from Rotten Tomatoes to IMDB. They also show you what’s new and noteworthy, what will be gone soon, etc.

They have lists for Amazon too.

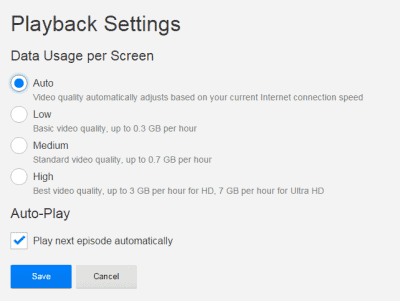

Manually Adjust Netflix Streaming Settings

If you want to adjust your data usage, you can set Playback Settings, under My Profile, in your Account.

It will play back video at whatever setting you put, regardless of your data capabilities.

If you want to adjust things on a video by video basis, hold Shift+Alt+Ctrl+S when the video is playing to reveal a menu that lets you adjust Audio Bitrate, Video Bitrate, and CDN. The Bitrate for audio and video manage the quality, the higher the bitrate the better the quality. CDN stands for Content Delivery Network and refers to the servers sending you the data. Switching them could improve, or hurt, performance.

On a Mac the key combination is Control+Shift+Option+S.

Review & Delete Your History

Hey, sometimes you want to know what you watched… or you don’t want someone to know you watched something. Or sometimes you don’t want a movie you half-watched messing up your recommendations. Right… the last one. 🙂

Go to netflix.com/viewingactivity to see your viewing history and click on the X to delete it.

How to Clear Your “Continue Watching” List

I never watch the credits of a movie, documentary or TV show and so my “Continue Watching” queue is an endless list of shows with 5 minutes left.

How do you clear or edit this Continue Watching list? The best way is to delete your viewing history – thus erasing that you ever watched it in the first place. You can always turn the show back on and let it run itself out, but who has time for that? Just delete it from your history and you’ll be rid of it. Instructions are above.

Browse Hidden Genres

Netflix has a whole slew of genres they don’t show to everyone, to see them you just need to load this URL:

Then go to this list of Netflix Genre IDs to find the one for you. (here’s an even longer list)

For example, if you want Animal Tales (5507), go to http://www.netflix.com/browse/genre/5507

Simple enough right?

Want some keyboard hot-key shortcuts?

Did you know you can control Netflix with just your keyboard?

- Pause: Space Bar or Enter

- Full Screen: F

- Exit Full Screen: F or Esc

- Volume: Up to increase, Down to decrease

- Mute: M

- Rewind/Fast Forward: Left and Right buttons will shift 10 seconds

If you like seeing technical stuff, hold Ctrl-Shift-Alt-D – you’ll see an overlay with a ton of information about your browser, the movie, the playback (bitrate, buffering, framerate) and other, mostly useless, information.

Ctrl-Shift-Alt-L will show you the log file.

Netflix Doesn’t Have It?

We have several streaming services so sometimes a show that isn’t available on Netflix might be available on Amazon Video. Or Hulu. Or Paramount+.

The best place to search is JustWatch, it’ll search all the other services to find out where you can get it. You can even set alerts for yourself.

I found a few services I’d never heard of before too, many of which can be accessed through your cable services (for example, See.it is a service available to Charter and Comcast xfinity)

Need a Fireplace?

If you need your TV to look like a fire place but don’t want to chop any wood, load this baby up. Now you have an hour of fire with no messy clean up, it even comes with Christmas-y/Holiday music, but you can mute that if you aren’t a fan. It even crackles!

Go forth and binge!

I’m gonna have to check out that instant watcher. I’m the ultimate binge watcher 🙂

I binge watch tv shows all the time to the point where I start missing them when the shows end!

Have you tried to use a Rite Aid gift card to buy another gift card (such as Netflix)?

I ran into an issue attempting to do something similar using a Walgreen’s gift card to buy a gas card thinking, “Hey 12% off gas…”

I have bought Netflix cards from Target, that’s about it.

I have tried this. Most stores won’t allow it.

Target will not allow you to purchase Netflix gift cards using Target gift cards. I read this today and purchased a target gift card just for this purpose and now I’m stuck with a Target gift card. Not the end of the world because i will eventually use it but I just figured I’d let everyone know this did not work for me.

Oh no! What did they say was the reason? (I amended the post to warn folks)

When I attempt to use the gift card it comes back with the following error message. “Sorry, you can’t use a Target GiftCard to purchase this type of card. Please choose another payment method.”

Ohhhh I wonder if you can do it in the store?

I just tried tonight and it worked in the store

Heeeeey! Fantastic!

For a recent post this bring some outdated news. The shortcut CTRL+Shift+Alt+S doesn’t work anymore, neither the Shift+Alt+Left Click that does the same thing. There was some developed extensions but Netflix is closing the siege on this. That is leading me to reavaliate my subscription on Netflix since even with a 100Mbps connection I’m still getting 480p videos and can’t force change it.

Hey. Not sure if this is still a good place to ask since it’s been so long, but If I get rid of my DVD account, does that shorten the available streaming titles?? I’d seen people’s lists in the past who didn’t have DVDs at all or they only had one a month, and they didn’t have the same streaming list as I did. They had way less titles. So I’m wondering if this is still the case.

Thanks, if you find this now days.

Terri

I don’t think the DVD account has an impact on your streaming.

I always try to pay things ahead of time. But with steaming services it’s all automatic. I didn’t know Netflix had gift cards, now with that I could buy the gift card and have that credit carry over. Very helpful, thanks.