Capital One Venture Rewards Card

Product Name: Capital One Venture Rewards Card

Product Description: Capital One Venture Rewards Card provides one of the most generous travel benefit packages in the credit card industry among credit cards with low annual fees.

Summary

Capital One Venture Card offers a sign-up bonus of 75,000 miles if you spend $4,000 on purchases within the first 3 months of opening the account, then follows that with 5X miles for every dollar spent on travel booked with Capital One Travel. The card then adds a multitude of other travel benefits, along with generous rewards miles on non-travel purchases. All this comes with a travel credit card with a very modest annual fee.

Overall

Pros

- 75,000 miles if you spend $4,000 on purchases within the first 3 months of opening the account.

- unlimited 2x miles per dollar on every purchase, every day.

- Multiple rewards redemption options.

- No foreign transaction fee.

Cons

- 5X miles on travel through Capital One Travel does not include airfare.

- $95 annual fee.

- 4% balance transfer fee, and 5% cash advance fee, though both are common in the credit card industry.

- Requires excellent credit to qualify for the card.

If you’ve been looking for a credit card that offers premium travel rewards and benefits – but without the high annual fee – look no further than the Capital One Venture Rewards Card. It combines high rewards, a large sign-on bonus, and travel perks available only with premium credit cards, all in a card with an annual fee of under $100.

At a Glance:

- Generous, easy to qualify for sign-on bonus.

- Earn 5X miles for every dollar spent on travel purchased through Capital One Travel.

- Packed with valuable travel benefits.

- High and unlimited rewards for other purchases.

- Multiple miles rewards redemption options, including transfers to other travel loyalty programs.

- Low annual fee.

Who Should Use the Capital One Venture Card?

While the Capital One Venture Card can be an excellent credit card choice for just about anyone – due to the combination of a very generous sign-on bonus and unlimited 2x miles per dollar on every purchase, every day – the card is designed specifically for frequent travelers.

That’s because the Capital One Venture Card provides enhanced travel benefits, like unlimited 5X miles on every dollar spent on travel booked through Capital One Travel. But the travel benefits don’t stop there. The Venture Card provides other valuable perks, like auto collision damage waiver, which is a benefit that is becoming increasingly uncommon even on travel cards, as well as no foreign transaction fees.

This is also an excellent choice if you want practically unlimited rewards redemption options. Capital One allows you to redeem rewards for new and previously booked travel purchases with Amazon.com or PayPal, gift cards to popular merchants, cash back in the form of a statement credit or a check, and other options.

While this card does have an annual fee, it’s only a fraction of the fee charged by competing credit card issuers that offer travel cards with this many benefits.

Alternatives to the Capital One Venture Card

| Chase Sapphire Preferred | Capital One Spark 1.5% Cash Select | Discover it Miles | |

|---|---|---|---|

| Sign up bonus | 60,000 Ultimate Rewards points if you spend $4,000 in purchases within the first three months | $500 if you spend $4,500 in the first 3 months from account opening | Automatic match on all miles earned at the end of your first year |

| Rewards | 5x points on travel purchased through Chase Ultimate Rewards, 3x points on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on everything else (plus a $50 annual Ultimate Rewards Hotel Credit) | unlimited 1.5% cash back on every purchase | Unlimited 1.5X miles every dollar on every purchase |

| 0% introductory offer | N/A | N/A | 0% APR for purchases and balance transfers for 15 months from the date of the first transfer |

| Annual fee | $95 | $0 | $0 |

| Learn More | Learn More | Learn More |

Table of Contents

- At a Glance:

- Who Should Use the Capital One Venture Card?

- Alternatives to the Capital One Venture Card

- What Is the Capital One Venture Card?

- Sign on Bonus

- Capital One Venture Rewards

- How to Redeem Capital One Venture Rewards

- 0% Introductory APR

- Other Card Benefits

- Capital One Venture Card Fees

- The Capital One Venture Card vs. Alternatives

- FAQs

- Should You Apply for the Capital One Venture Card?

What Is the Capital One Venture Card?

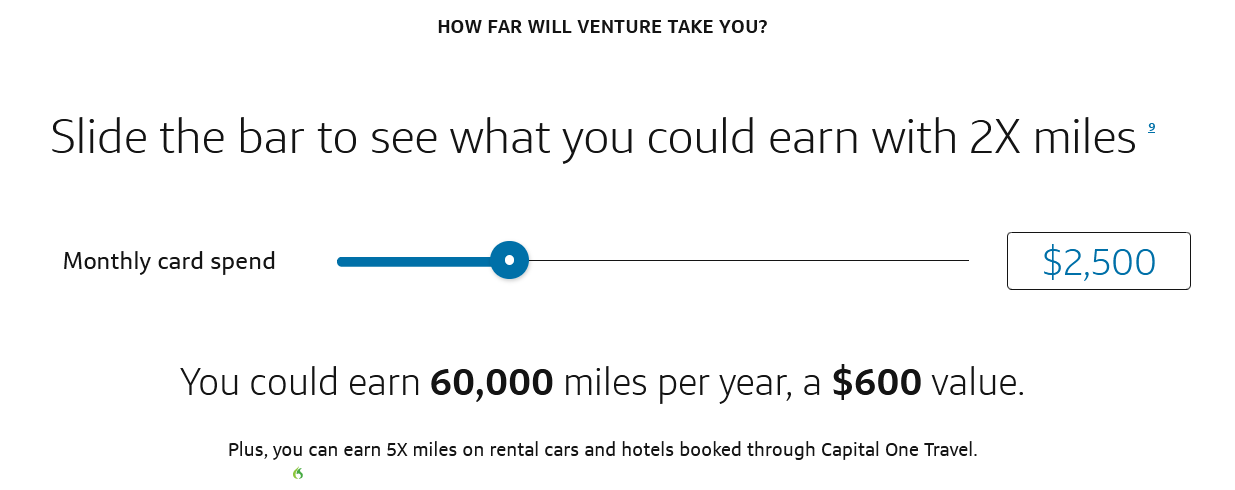

Capital One Venture Card is a rewards credit card specifically focusing on travel-related rewards and benefits. Though the card pays unlimited 2x miles per dollar on every purchase, every day, you can earn 5X miles for every dollar spent on purchases through Capital One Travel.

From there, the card also provides valuable travel benefits, including a credit of up to $120 toward Global Entry or TSA PreCheck, and auto collision damage waiver on car rentals. But the whole offer starts with a very generous sign-on bonus worth hundreds of dollars.

You’ll also enjoy 24/7 customer service, the ability to choose your due date, credit monitoring through Capital One’s CreditWise free credit monitoring service, security and account alerts, virtual cards, and $0 fraud liability protection against unauthorized charges.

All of those rewards and benefits come packed on a credit card with no foreign transaction fees and an annual fee of just $95.

Learn More about the Capital One Venture Rewards Credit Card

Sign on Bonus

The Capital One Venture Card starts you off with a very generous sign-on bonus, enabling you to earn 75,000 miles if you spend $4,000 on purchases within the first 3 months of opening the account. That translates into miles worth $750, or nearly $0.19 for every dollar spent.

The bonus will be redeemable within two billing cycles after it has been earned. Like other Capital One rewards, your bonus miles never expire as long as your account remains open.

Current Capital One credit card customers are not eligible for this card or the bonus if they have received a new cardmember bonus on the same card within the past 48 months.

Capital One Venture Rewards

Capital One Venture offers three rewards level categories:

- 5X miles on every dollar spent on travel purchases made through Capital One Travel. This includes hotel, car rentals, and vacation rentals – but not airfare purchases.

- unlimited 2x miles per dollar on every purchase, every day, including airfare purchases.

- 5X miles on Capital One Entertainment purchases, providing you with access to concerts, sporting events, and dining with exclusive presales, tickets, and suite access.

How to Redeem Capital One Venture Rewards

Capital One Venture Rewards are unlimited and won’t expire for the life of the account. They can be redeemed through any of the following methods:

- Travel booked through Capital One Travel.

- Reimbursement for recent travel purchases using your Venture card.

- Gift cards with your favorite merchants.

- Cash, in the form of either a statement credit or a check.

- For eligible PayPal purchases at millions of online merchants.

- To shop on Amazon.com.

You can also transfer your rewards miles to one of 16 travel loyalty programs, some of which include:

- Aeromexico Club Premier

- Air Canada Aeroplan

- Avianca Life Miles

- British Airways Executive Club

- Choice Privileges

- Emirates Skywards

- Qantas Frequent Flyer

- Singapore Airlines KrisFlyer

- TAP Miles&Go

- Virgin Red

- Wyndham Rewards

You’ll receive 1,000 miles or points when you transfer 1,000 Capital One miles to most participating travel rewards partners.

0% Introductory APR

Capital One Venture does not offer a 0% introductory APR at this time.

Other Card Benefits

Capital One Venture Card also comes with a laundry list of other valuable perks and benefits:

- Credit of up to $120 toward Global Entry or TSA PreCheck.

- Hertz Five Star status, entitling you to free status upgrades, a wider selection of rental cars, and the ability to skip the line.

- Average savings of 15% on flights with price prediction from Capital One Travel.

- Auto rental collision damage waiver when you charge a car rental, using the card.

- Elevate your stay – receive a $50 experience credit to use on Lifestyle Collection bookings at unique hotels.

- 24-hour travel assistance.

- Automatic accident insurance for a covered loss at no extra charge when you purchase airline tickets using the card.

- No foreign transaction fees.

- Capital One Shopping, a free browser extension that automatically applies the best available coupon codes at check out, and alerts you when prices drop on items you’ve viewed or purchased.

- Capital One Offers give you exclusive access to earn statement credits when you shop at popular online retailers.

- Extended warranty on purchases made using the card, at no additional cost.

- Capital One Dining gives you access to unique dining experiences in major cities around the world.

- 50% off handcrafted beverages every day at Capital One Cafes.

Learn More about the Capital One Venture Rewards Credit Card

Capital One Venture Card Fees

Like most credit cards, Capital One Venture Card charges some fees. Common ones are as follows:

- Annual fee: $95

- Balance transfer fee: 4% of the amount transferred

- Cash advance fee: the greater of $5 or 5% of the amount of each advance

- Late fee: $40

- Foreign transaction fee: 0

The Capital One Venture Card vs. Alternatives

Chase Sapphire Preferred

Chase Sapphire Preferred comes the closest to matching Capital One Venture. It’s also a travel specific credit card, offering 5x points on travel purchased through Chase Ultimate Rewards, 3x points on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on everything else (plus a $50 annual Ultimate Rewards Hotel Credit), as well as no foreign transaction fees, auto rental coverage, and extended warranty protection.

However, Chase offers something the Venture card does not, with a 25% rewards points enhancement when points are redeemed for travel through Chase Travel. In that way, the 60,000 point sign-on bonus will be worth $750.

In addition, on each account anniversary, you’ll earn bonus points equal to 10% of your total purchases made the previous year. That means $30,000 in purchases using the card will translate into an additional 3,000 bonus points.

Chase Sapphire Preferred also throws in some additional travel benefits, like trip cancellation and interruption insurance, baggage delay insurance, and travel and emergency assistance.

Read our full Chase Sapphire Preferred Review

Chase Button

Capital One Spark 1.5% Cash Select

Capital One Spark 1.5% Cash Select is something like a cousin to the Capital One Venture Card, except it’s designed specifically for businesses. It’s also a travel-centric card, offering unlimited 1.5% cash back on every purchase. Though the non-travel rewards are less generous than they are for Capital One Venture, Spark 1.5% Cash Select does pay rewards in cash. That can be either a statement credit or a check.

The sign-on bonus is also less generous than it is for the Capital One Venture Card at $500 if you spend $4,500 in the first 3 months from account opening. But once again, that bonus will be paid in cash, not points. As a business card, you can offer free employee cards with set spending limits, assign account managers, maintain purchase records, and get year-end summaries.

Learn more about Capital One Spark Cash Select

Discover it Miles Card

If you prefer a travel credit card with a much simpler reward plan, Discover it Miles is worth checking out. Though it doesn’t pay an enhanced benefit on travel purchases, it does offer unlimited 1.5X miles on every dollar on all purchases.

It doesn’t offer a formal sign-on bonus, the way the Capital One Venture Card does, it does provide an automatic 100% match of all miles earned in your first year. That eliminates the need to meet a spending quota within the first three months of owning the card.

Discover it Miles offers an important benefit Capital One Venture Card doesn’t have, which is a 0% introductory APR on purchases and balance transfers for 15 months In addition, the card has no annual fee, and no foreign transaction fees. Your miles can be redeemed toward travel purchases or for statement credits against your bill. Your miles never expire, even if you close your account.

Discover button

FAQs

The Capital One Venture card can be an excellent choice for frequent travelers.

The welcome offer starts with 75,000 miles if you spend $4,000 on purchases within the first 3 months of opening the account. Rewards include unlimited 2x miles per dollar on every purchase, every day. There is also no foreign transaction fee.

All these benefits are included in a credit card with an annual fee of just $95. Some cards offering this type of benefits package have much higher annual fees.

Capital One indicates applicants need “excellent” credit to be approved for the Venture card. They define excellent credit as follows:

“I’ve never declared bankruptcy or defaulted on a loan; I haven’t been more than 60 days late on any credit card, medical bill, or loan in the last year; I’ve had a loan or credit card for 3 years or more with a credit limit above $5,000.”

Capital One doesn’t issue specific guidelines on the minimum required credit score. However, various online sources are indicating an effective minimum FICO Score of between 670 and 700.

As indicated in the answer to the previous question, Capital One uses a subjective definition of what constitutes acceptable credit.

Should You Apply for the Capital One Venture Card?

Several premium credit cards offer the kinds of travel rewards and benefits provided by the Capital One Venture Card. However, those cards usually have annual fees of $500 or more, making them suitable only for very frequent travelers.

But if you are a not-so-frequent traveler, and want to enjoy premium rewards and benefits on a card with a low annual fee, apply for the Capital One Venture Card today.