When you are living paycheck to paycheck, breaking out of that cycle seems impossible.

You’re always playing catch up or you’re one emergency away from being sent back to the start. Or worse.

But it is doable, and believe it or not, you don’t even have to find ways to earn more money to do it. Making more can help but there are plenty of people who make sky high incomes and still live paycheck to paycheck. Your income isn’t actually a factor here.

Think of it this way… you are already living on your current income. Living paycheck-to-paycheck is sometimes only about the timing of our cash flow.

Table of Contents

Get Serious about Budgeting

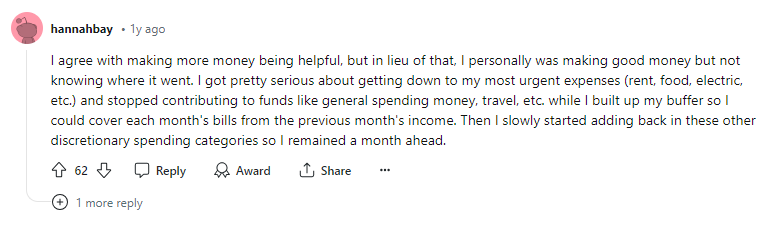

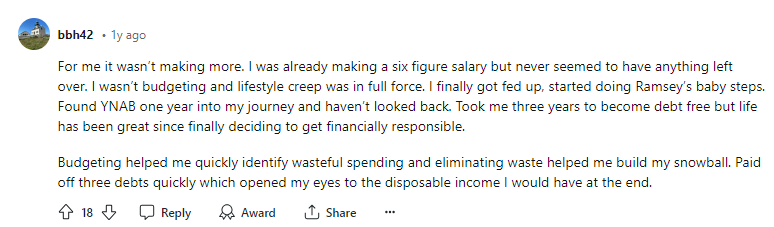

Understanding where your money is going is step one. In this Reddit thread, people shared what helped them break the cycle, and a lot of them mentioned budgeting.

You’ll need to build a buffer between getting your paycheck and spending it. And the way to do that is to spend a little less than your whole check each pay period. You don’t have to save much, even $5 a paycheck will be a step in the right direction.

One budgeting tool that is extremely useful for breaking the paycheck-to-paycheck cycle is YNAB. The key theory of YNAB, and one of it’s secrets to success, is to live on last month’s income by giving every dollar a job.

The paychecks you receive this month go towards next month’s budget.

This means that on the first of the month, you have the money you will need for the whole month sitting in your checking account with a plan for how it will be used.

When you reach this point, the timing of your paychecks arriving and your bills being due will no longer matter. You’ll have everything you need to get through the month.

Here’s our full YNAB review if you want to learn more.

Another benefit of budgeting that I don’t feel is discussed very often is that a budget allows you to take advantage of any boons or windfalls you receive. Being able to take full advantage of these opportunities to get ahead will only make things easier going forward.

Without a budget, it’s easy to use a bonus or tax return to splurge a little and miss the opportunity to get ahead simply because you don’t see the benefit laid out clearly before you.

OK – all of this sounds too handy wavy and simple – how do you execute this in real life?

✨ Related: 4 Different Budgeting Strategies to Try this Year

Build a One Paycheck Buffer

While getting a full month ahead is the ultimate goal, it may feel a bit daunting. So, first, set out to get one paycheck ahead.

Set aside whatever you can, even if it’s a small amount, and build up a one-paycheck buffer in your checking account. Rely on your budgeting to ensure that this stays as a buffer and doesn’t get spent without being replenished on your next check.

Just this small-ish buffer will give you some wiggle room in the timing of your spending, and you will start to feel more in control of your finances.

If you get paid weekly or bi-weekly, there are some months when you get an extra paycheck. That is the perfect time to build this buffer. If you want to build it more quickly, consider things like selling some of the stuff you no longer use, canceling some subscriptions you don’t need, and picking up some odd jobs or overtime at work. Again, every little bit helps.

Once you have a one-paycheck buffer, start working on getting a full month ahead in your budgeting.

✨ Related: How to Organize your Bills: 8 Helpful Tips

Start Paying Down Debt

Once you are budgeting one month ahead, you can focus on paying down debt.

Paying down debt is one of the most powerful things you can do. Add up all your monthly payments and imagine if you had that money in your budget every month. You can see that it would be a powerful tool.

The debt snowball is a great way to pay down debt, and combine that with the power of YNAB and you are well on your way to getting ahead. Here are some debt snowball tools to help get you started.

Find a Support Group

This can be online, such as a Facebook group or Reddit, or be with one or two of your local friends. The important part is finding someone you can trust to talk to because the journey will be difficult. You’ll need some support when things don’t go your way and someone cheerleaders to help you celebrate when they do.

Breaking the cycle isn’t easy but it’s doable, especially if you have important people around you to help.

Summary

It is possible to break the paycheck-to-paycheck cycle, even without increasing your income. You’ll want to start by budgeting so you have a clear view of how you are spending your money and then start putting something aside, no matter how small, to begin to build a buffer.

Aim to build a buffer of one paycheck and then build that up to being able to fund next month’s budget with this month’s income. Once you have done that, you can start paying off debt and really begin to make an impact on your finances.